- Find a Brokerage Firm

- Find a Listed Company

- Contact Us

- Connect PSX

The audio is loading, please wait ...

Published On: June 01, 2022

In the rigmarole of our daily lives, we usually forget the importance of savings and investing for the future. We are busy paying the due installments against our car, house, annual kitty, and bills, amongst other expenses. At the same time, we have to save for our children, their education, their marriages and for all that entails us being “responsible” parents.

But what is it that we have really forgotten to think over in this rat-race of life? We seem to have forgotten what will happen once we retire and once the proverbial tap starts to run dry. How will we meet our expenses then? There will be medical bills, utility bills and insurance bills to be paid. There could be expenses incurred for any foreign trips, social gatherings and invitations attended. This is just an example of the number of expenses that we may well have to face when we retire and are on our own. The time is now to think of ourselves and our welfare in our post-retirement age!

Considering the ever increasing expenses, the impact of inflation and the decrease in purchasing power of our currency, how does one beat all these negatives, and still come out on top with enough funds to cover expenses post-retirement? The answer lies in saving and investing. But with so many investment instruments and asset classes to choose from, which one would be optimal, which one would protect us from the loss of purchasing power and shield us from inflation, yet leave us enough to help us meet our daily expenses?

Enter the Stock Market! Financial instruments such as mutual funds and equities have not only provided good returns but have also shielded investors from hard-hitting effects of inflation in the longer term. We have seen dividend yields of 5.7%* for last one year and compounded rate of return of 15.13%** of KSE 100 Index stocks over the last 15 years. We can avail these returns for ourselves and have enough savings by the time of retirement. However, we must save and invest for the long term to be able to earn the dividends and returns that we seek to put us in a comfortable position in future.

Consider you are under 35 years of age and earn a salary of Rs 80,000/- p.m. So, what is your target date? Presuming it is 65 years of age, you have 30 years to save and invest. So, can you cut back on your expenses for now? Is it necessary to eat outside and attend every social invitation? Can you save on electricity bills and petrol costs? If there is a possibility to save funds to the tune of Rs 6000/- p.m., then you are off to a good start. If you can count on some familial support, as is generally the case in our society, then you are on the right track to save and invest on the basis of these additional funds. Suppose you get a stipend of Rs 7000/- p.m. from your parents/ family support, you now have a total of Rs 13,000/- p.m. saved with yourselves. Saving these funds (Rs 13,000/- p.m.) for around a year can leave you with an amount of Rs 160,000/- to start investing.

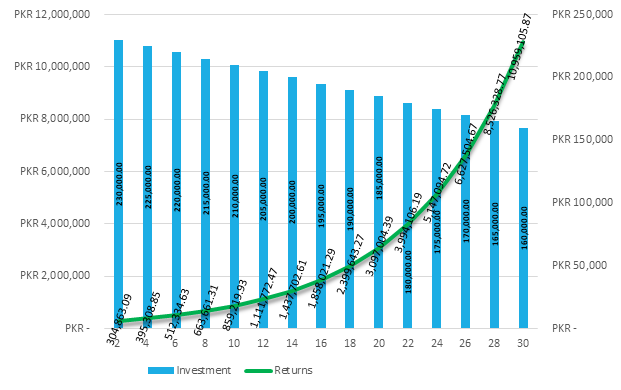

Armed with this amount of money, you can buy the minimum lot of 500 shares of a diversified portfolio of companies listed on the KSE-100 Index. You can then let the investment grow at the compounded annual rate of return of 15.13%** per annum, assuming the rate remains constant. Furthermore, as your salary increases, if you save an incremented amount every two years, and invest the same until retirement, you can earn compounded returns on these as well. These savings and investments can leave you with a combined total of Rs 4.79 Crores at your retirement @ 15.13%** CAGR. The progression of your investment and its returns is illustrated in the graph below.

So with an initial investment of Rs 160,000, you can start investing in the Stock Market. Subsequently, if it is not easy for you to save every year and as your salary increases, then every two years you can save an incremented amount and invest the same until retirement. This periodic saving and investing for a period of thirty years, until retirement, can leave you with an amount of Rs 4.79 Crores.

Even if you have a small amount of saving, and if you start early, you can save enough for the rainy days at your age of retirement. So investing at the right time in KSE-100 Index stocks might be the optimal way forward for you.

Disclaimer:

The contents of this article comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions.

*Source: Bloomberg)

**(Compounded Annual Growth Rate of KSE 100 Index stocks between 31/12/03-31/12/18) (Source: Bloomberg)